Plan Your Money Throughout The Year

Why is important to plan your money throughout the year?

Planning your money throughout the year is one of the most critical areas you must deal with in life! It can also be one of the scariest and most stressful things we must do. Not all of us are happy discussing money, which can sometimes be a barrier for some people. We all need to get over the stigma of money and have a more positive attitude toward it. Try to work with your finances, not against them. Getting on top of your finances can be a great way to get on top of your money.

Being confident about your finances for the year is an essential job. Finding the time throughout the year will allow you to budget all areas of your finances. Plus, it will enable you to plan where and when you spend your money. We find it easy these days to pay with our plastic money, but we must remember how easy it is to get into debt. Because it is easy to spend plastic money, it is okay. But the consequence is that you must find a way to repay it long-term.

Clear structured plan throughout the year

A clear, structured plan for your finances will help you stop spending plastic money, stay on track, and stay out of debt. Plus, when you purchase something, you pay with your hard-earned cash, not plastic money. Buying an item that you have worked hard and saved for is a great feeling, unlike the sense of being in debt.

If you are in a relationship where you share responsibility when paying the bills, like household bills, the responsibility is shared. Additionally, you both need to be very honest with each other. You have come together as a team and do not work against each other. You are together because you want the same things, so be a team. Share your money, and make it work for both of you.

So take a look at these clear, simple six steps to plan your money throughout the year:

Step One - Do Not Be Afraid of your money

Be honest with your money, and stop fearing it! That is easy, but I have been where you have been. I was always scared to look at my bank, what was in my bank, and how I would pay the bill. Also, seeing that I had no money. The worst thing you can do is be afraid of your money. Best thing to do is have a healthier relationship with your money and not fear it. Build a more positive relationship and become more confident with the finances.

If you have a partner, do this together, which can be more comforting. With someone to lean on, you can learn together to have a better financial relationship.

Step Two - In & Out Goings plan your money throughout the year

However, one of the most important things you must do is sit down be true to your finances and plan your money throughout the year. Looking at all your monthly income in the house, which can be your wages from both you and your partner, child benefits, or any benefits you may receive.

Moving on to all your outgoings, which can be:

- Mortgage/ Rent

- Monthly household bills – Water, Gas & Electric, council tax and Broadband

- TV licenses including TV subscriptions like Sky, Netflix, Disney Plus, and more

- Home and life insurance

- Food Bill

- Car and other finances

- Car bills – Fuel, Tax, Car insurance, servicing, and breakdown cover

- Saving – pensions, personal and kids savings

- Pocket money kids

- Kids clubs

- Mobile phones

- Birthday fund

- Christmas fund

- Days out

- Clothing and shoes

- Emergency fund

- Savings Challenge

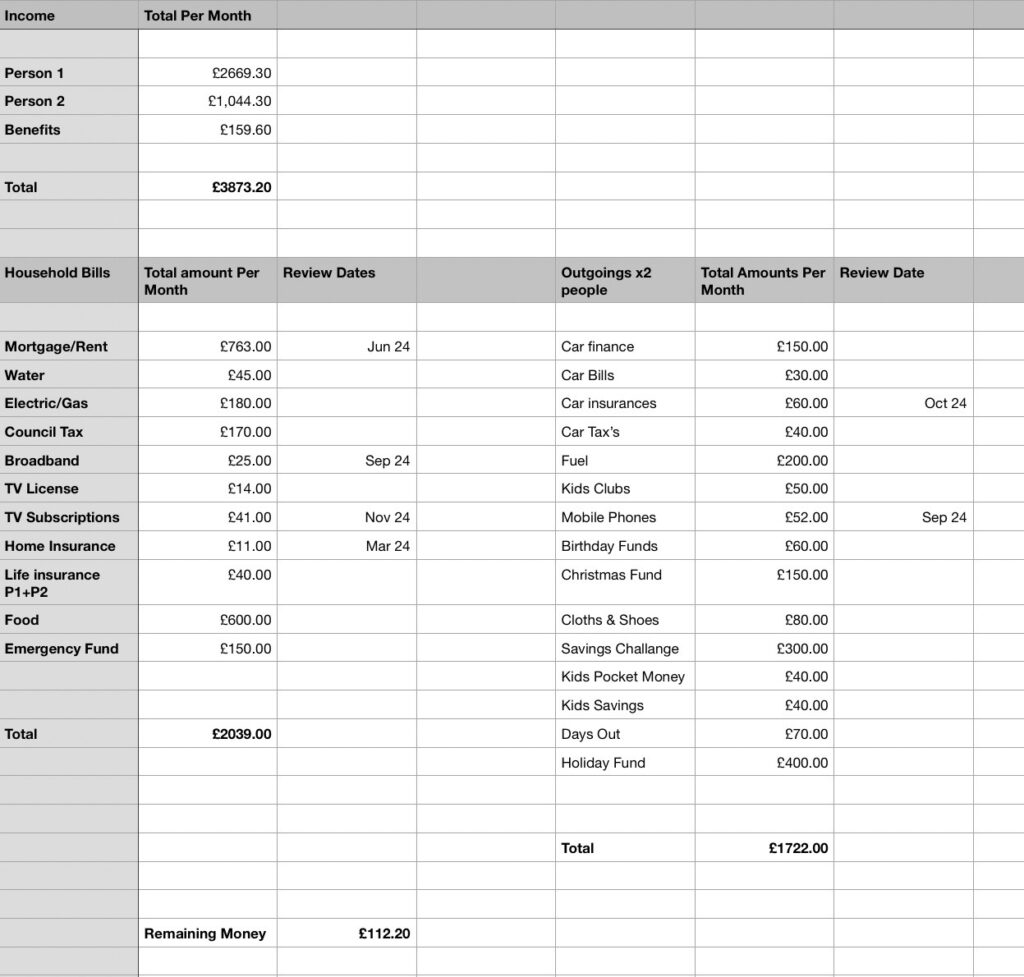

Working with these areas of planning your money throughout the year, you must pop them into a spreadsheet. Allowing you to see what is coming in and out – here is an example of a sheet from Plan Your Money Throughout the Year:

Step Three - Get Good Deals with planning your money

Now, you have all your finances in spreadsheets, giving you a clearer picture of your money. Start analyzing your outgoings and see what you can improve. Find better deals on TV subscriptions, Broadband, Mobile, and insurance. Work one by one down your spreadsheet and see where you can get a better deal. Now, this will allow you to cut down and make your money go further.

TIPS

Braking down your spreadsheet, have dates when your deals are ending. Then, a month before your deal ends, make a date to research for a better deal. It is essential to do a month before. Researching a week or a few days before may be a risk. Sourcing a deal a month early classes as a safe person with your finances leads to better deals available as the risk is lower. Popping an earlier date in your phone reminder will give you a head start on your search. When shopping for deals, use all the comparison sites, not just one. By researching all areas, you can get the best deal. Sometimes, you can get extras like cashback, cinema tickets, and more. Shop about, or if you like your provider, call them. Try to discuss your deal and bring down the price. It is worth a try.

Step Four - How To Keep Your Money throughout the year

This area will be different for different people. Some people love to be able to hold their cash and have envelopes or files to divide their cash. Provides you help to see where their money goes for each bill or savings. Most of the time, we still need to get the money in the bank to pay these bills, as most people pay by direct debit. Cash in the home, especially where you have saved, is very vulnerable, so we must be mindful. Conversely, some people pay their bills from their bank account and keep them in their savings account.

Separate Bank Accounts

A healthy way to manage your finances is if you and your partner have separate bank accounts where your wages or benefits go. In addition, you should have a joint account for your household bills like rent/mortgage and any bills related to home running. You both signed into living with each other and being responsible for the bills. Then you know you have paid your part to the joint account. Looking at the remaining part of your wages, it is up to you to manage how you spend and save.

Right Account for You?

Finding new ways to manage money, kids today want their money in a bank or finance app with a card or phone to pay, depending on age. Researching finance apps for kids, and there are many. I found one Hyper Jar that ticked all the boxes—free sign-up plus no subscription each month. Kids have an app on their devices. Easy to send money and manage their spending, having pots to spend and save in. Your account has ten saving pots and other perks like gift cards.

This account helps me structure money well, stopping me from saving in envelopes. I divide my money into different pots for different times of the year and link the pots when spending is needed. For example, I keep all my Christmas budget in one pot, and then when it comes to that time of the year, I spend on that.

Savings Accounts

Having two savings accounts might be an excellent way to go. Firstly, instant access so you can get your money instantly if needed. Secondary a savings account where it takes a few days or longer to get to your money. The interest you gain in the instant savings account is much smaller than if you have a savings account that takes longer to draw out—creating an excellent incentive to avoid drawing the money out. Having both savings accounts helps if you need to find the extra cash from month to month. Hit your small interest savings account without harming your more extensive interest account.

Step Five - Review Your Spending Habits throughout the year

Review your spending habits regularly. By doing this, it should help keep you out of debt. We should only spend money if we have pennies. Also, it is a great way to keep a look at your bank account. Make sure that it’s you spending your money, not anyone else, so keeping a good eye on your account can make you feel more confident and understand your money. Banks today have excellent facilities to show you how you spend your money, and we should use them more. At the same time, checking our spending habits at least every month. Firstly, this is to keep you out of debt. Secondly, by checking your account regularly, you can see if you can reduce your spending and plan to improve your spending habits.

Step 6 - Saving Challenges by planning your money throughout the year

Saving challenges have become very popular over the years, and they are a great way to save some pennies. As the years have passed, there have been so many saving challenges.

What is the right one for you?

Saving is a great way to stay out of debt; we all should do this wherever possible. Saving for Christmas, birthdays, and emergencies should be a must. These are areas where you will have to spend at some point throughout the year. However, having the money to hand instead of borrowing money means we are only paying the money we have instead of getting into debt.

There are many saving challenges, from keeping 1p a day and £1 a day to the £ 25-month challenge. The list is endless. All saving challenges should be personal to you and what you can afford.

One of the savings challenges with plan your money throughout the year

One of the savings challenges we decided to do has taken us three years but is working well. In the first year, you must look at all your monthly spending. Then, for every £1 you spend, you save a penny, so if your household spending, for example, in the month is £4500.00, you need to keep 1p per £1. At the end of the month, you would have saved £45.00, and for the year, you would have saved £540.00.

Second year, we ramped up the challenge, saving 5% of what we spent, so again, £4500.00, we would need to save £225 per month, leading to £2,700.00 a year.

Third year we have been working towards saving 10% of what we spend, so £4500.00 will be £450.00 per month. That is 10p for every £1 we spend at home, so at the end of the year, we have saved £5,400.00.

Knowing that we have got to this saving challenge, this is doable for our family, and we find this will not put us into trouble, so we are happy that we have to save 10% each month. Making sure we have saved for all the other stuff and keep out of debt. As a couple saving this money, the responsibility comes to both of you. Maybe you save half each, or if one of you works part-time and one full-time, the part-time partner would save a quarter, and the full-time save three quarters.

Savings challenges are Personal to each person

Challenges are personal to each household, so discuss what is great for your family.

Always keep your challenge under review. Some months, you may need help to do the challenge or save a bit, but less of the challenge. That’s okay. Finding you hit a wall, save whatever you can.

Think about not spending the money once you have saved it and keeping it for a rainy day. Why not put your money into an account that can earn money, like a high-interest savings account or an ISA? Get more for your hard-earned savings to keep earning money for you.

So why not sit down and decide on a savings challenge, start saving, and see how much money you can save? Challenge yourself for the year after to gain even more savings. Happy savings!

Along with keeping our money in check and not being afraid to look at it, we can build a great relationship with our finances. Lastly, We Should Organize all our bills, keep them in check, and know exactly where we are spending. We should ensure we get the best deals and make our money go further to save our leftover pennies. Gain some extra cash in the bank. Why not work on your six steps and be more confident with the money that comes into the home by planning your money throughout the year?